[ad_1]

The notes are being issued by Royal Financial institution of Canada (“RBC”). There are vital variations between the notes and a standard debt safety, together with completely different funding dangers and sure

extra prices. See “Danger Elements” and “Extra Danger Elements” starting on web page TS-6 of this time period sheet and starting on web page PS-6 of product complement EQUITY ARN-1.

The preliminary estimated worth of the notes as of the pricing date is predicted to be between $9.05 and $9.55 per unit, which is

lower than the general public providing worth listed under. See “Abstract” on the next web page, “Danger Elements” starting on web page TS-6 of this time period sheet and “Structuring the Notes” on web page TS-12 of this time period sheet for extra info. The

precise worth of your notes at any time will replicate many elements and can’t be predicted with accuracy.

Not one of the Securities and Change Fee (the “SEC”), any state securities fee, or another regulatory physique has accepted or disapproved of those securities or decided if this Observe

Prospectus (as outlined under) is truthful or full. Any illustration on the contrary is a prison offense.

|

Per Unit |

Whole |

|

|

Public providing worth(1) |

$10.000 |

$ |

|

Underwriting low cost(1) |

$0.175 |

$ |

|

Proceeds, earlier than bills, to RBC |

$9.825 |

$ |

| (1) |

For any buy of 300,000 items or extra in a single transaction by a person investor or in mixed transactions with the investor’s family on this providing, the general public providing worth and the underwriting low cost will likely be $9.950 |

The notes:

|

Are Not FDIC Insured |

Are Not Financial institution Assured |

Could Lose Worth |

BofA Securities

January , 2021

Abstract

The Accelerated Return Notes® Linked to the VanEck Vectors® Gold Miners ETF, due March , 2022 (the “notes”) are our senior unsecured debt securities. The notes usually are not assured or

insured by the Canada Deposit Insurance coverage Company or the U.S. Federal Deposit Insurance coverage Company or secured by collateral. The notes will rank equally with all of our different unsecured and unsubordinated debt. Any

funds due on the notes, together with any compensation of principal, will likely be topic to the credit score danger of RBC. The notes usually are not bail-inable notes (as outlined within the prospectus complement). The notes

present you a leveraged return, topic to a cap, if the Ending Worth of the Market Measure, which is the VanEck Vectors® Gold Miners ETF (the “Underlying Fund”), is bigger than the Beginning Worth. If the Ending Worth is lower than the

Beginning Worth, you’ll lose all or a portion of the principal quantity of your notes. Any funds on the notes will likely be calculated primarily based on the $10 principal quantity per unit and can depend upon the efficiency of the Market Measure, topic to our

credit score danger. See “Phrases of the Notes” under.

The financial phrases of the notes (together with the Capped Worth) are primarily based on our inside funding charge, which is the speed we might pay to borrow funds by means of the issuance of market-linked notes and the

financial phrases of sure associated hedging preparations. Our inside funding charge is often decrease than the speed we might pay after we difficulty standard fastened or floating charge debt securities. This distinction in funding charge, in addition to the

underwriting low cost and the hedging associated cost described under, will scale back the financial phrases of the notes to you and the preliminary estimated worth of the notes on the pricing date. Because of these elements, the general public providing worth you pay to

buy the notes will likely be better than the preliminary estimated worth of the notes.

On the quilt web page of this time period sheet, we’ve offered the preliminary estimated worth vary for the notes. This preliminary estimated worth vary was decided primarily based on our and our associates’ pricing

fashions, which take into accounts our inside funding charge and the market costs for the hedging preparations associated to the notes. The preliminary estimated worth of the notes calculated on the pricing date will likely be set forth within the remaining time period

sheet made accessible to buyers within the notes. For extra details about the preliminary estimated worth and the structuring of the notes, see “Structuring the Notes” on web page TS-12.

|

Issuer: |

Royal Financial institution of Canada (“RBC”) |

|

|

Principal Quantity: |

$10.00 per unit |

|

|

Time period: |

Roughly 14 months |

|

|

Market Measure: |

The VanEck Vectors® Gold Miners ETF (Bloomberg image: “GDX”) |

|

|

Beginning Worth: |

The Closing Market Value of the Market Measure on the pricing date |

|

|

Ending Worth: |

The common of the Closing Market Costs of the Market Measure instances the Value Multiplier on every calculation day occurring throughout the Maturity Valuation Interval. The |

|

|

Value Multiplier: |

1, topic to adjustment for sure occasions referring to the Market Measure, as described starting on web page PS-26 of product complement EQUITY ARN-1. |

|

|

Participation Fee: |

300% |

|

|

Capped Worth: |

[$12.83 to $13.23] per unit, which represents a return of [28.30% to 32.30%] over the principal quantity. The precise Capped Worth will likely be decided on the pricing date. |

|

|

Maturity Valuation Interval: |

5 scheduled calculation days shortly earlier than the maturity date. |

|

|

Charges and Fees: |

The underwriting low cost of $0.175 per unit listed on the quilt web page and the hedging associated cost of $0.05 per unit described in “Structuring the Notes” on web page TS-. |

|

|

Calculation Agent: |

BofA Securities, Inc. (“BofAS”). |

|

Redemption Quantity Dedication |

|

On the maturity date, you’ll obtain a money cost per unit decided as follows:

|

The phrases and dangers of the notes are contained on this time period sheet and within the following:

Because of the completion of the reorganization of Financial institution of America’s U.S. broker-dealer enterprise, references to Merrill Lynch, Pierce, Fenner & Smith Included (“MLPF&S”) within the accompanying prospectus

complement, as such references relate to MLPF&S’s institutional companies, ought to be learn as references to BofAS.

These paperwork (collectively, the “Observe Prospectus”) have been filed as a part of a registration assertion with the SEC, which can, with out price, be accessed on the SEC web site as indicated above or obtained

from MLPF&S or BofAS by calling 1-800-294-1322. Earlier than you make investments, you must learn the Observe Prospectus, together with this time period sheet, for details about us and this providing. Any prior or contemporaneous oral statements and another written

supplies you might have obtained are outmoded by the Observe Prospectus. Capitalized phrases used however not outlined on this time period sheet have the meanings set forth in product complement EQUITY ARN-1. Except in any other case indicated or except the context requires

in any other case, all references on this doc to “we,” “us,” “our,” or comparable references are to RBC.

Investor Issues

You might want to contemplate an funding within the notes if:

| ◾ |

You anticipate that the Market Measure will improve reasonably from the Beginning Worth to the Ending Worth. |

| ◾ |

You’re prepared to danger a lack of principal and return if the Market Measure decreases from the Beginning Worth to the Ending Worth. |

| ◾ |

You settle for that the return on the notes will likely be capped. |

| ◾ |

You’re prepared to forgo curiosity funds which can be paid on standard curiosity bearing debt securities. |

| ◾ |

You’re prepared to forgo the dividends or different advantages of straight proudly owning shares of the Underlying Fund or the securities held by the Underlying Fund. |

| ◾ |

You’re prepared to just accept a restricted or no marketplace for gross sales previous to maturity, and perceive that the market costs for the notes, if any, will likely be affected by numerous elements, together with our precise and perceived creditworthiness, our |

| ◾ |

You’re prepared to imagine our credit score danger, as issuer of the notes, for all funds underneath the notes, together with the Redemption Quantity. |

The notes is probably not an applicable funding for you if:

| ◾ |

You consider that the Market Measure will lower from the Beginning Worth to the Ending Worth or that it’ll not improve sufficiently over the time period of the notes to offer you your required return. |

| ◾ |

You search principal compensation or preservation of capital. |

| ◾ |

You search an uncapped return in your funding. |

| ◾ |

You search curiosity funds or different present earnings in your funding. |

| ◾ |

You need to obtain dividends or have the opposite advantages of straight proudly owning shares of the Underlying Fund or the securities held by the Underlying Fund. |

| ◾ |

You search an funding for which there will likely be a liquid secondary market. |

| ◾ |

You’re unwilling or are unable to take market danger on the notes or to take our credit score danger as issuer of the notes. |

|

We urge you to seek the advice of your funding, authorized, tax, accounting, and different advisors earlier than you spend money on the notes. |

Hypothetical Payout Profile and Examples of Funds at Maturity

The graph under relies on hypothetical numbers and values.

Accelerated Return Notes®

This graph displays the returns on the notes, primarily based on the Participation Fee of 300% and a hypothetical Capped Worth of $13.03 per unit (the midpoint of the Capped Worth vary of [$12.83 to $13.23]). The inexperienced line displays the returns on

the notes, whereas the dotted grey line displays the returns of a direct funding within the Market Measure, excluding dividends.

This graph has been ready for functions of illustration solely.

The next desk and examples are for functions of illustration solely. They’re primarily based on hypothetical values and present hypothetical returns on the notes. They

illustrate the calculation of the Redemption Quantity and complete charge of return primarily based on a hypothetical Beginning Worth of 100, the Participation Fee of 300%, a hypothetical Capped Worth of $13.03 per unit and a spread of hypothetical Ending Values. The precise quantity you obtain and the ensuing complete charge of return will depend upon the precise Beginning Worth, Ending Worth, Capped Worth, and whether or not you maintain the notes to maturity. The next examples don’t

keep in mind any tax penalties from investing within the notes.

For latest precise costs of the Market Measure, see “The Underlying Fund” part under. The Ending Worth won’t embrace any earnings generated by dividends paid on the Market Measure, which you’d in any other case be entitled

to in the event you invested within the Market Measure. As well as, all funds on the notes are topic to issuer credit score danger.

|

Share Change from the Beginning Worth to the Ending Worth |

Redemption Quantity per Unit |

Whole Fee of Return on the Notes |

||||

|

0.00 |

-100.00% |

$0.00 |

-100.00% |

|||

|

50.00 |

-50.00% |

$5.00 |

-50.00% |

|||

|

80.00 |

-20.00% |

$8.00 |

-20.00% |

|||

|

90.00 |

-10.00% |

$9.00 |

-10.00% |

|||

|

94.00 |

-6.00% |

$9.40 |

-6.00% |

|||

|

97.00 |

-3.00% |

$9.70 |

-3.00% |

|||

|

100.00(1) |

0.00% |

$10.00 |

0.00% |

|||

|

102.00 |

2.00% |

$10.60 |

6.00% |

|||

|

103.00 |

3.00% |

$10.90 |

9.00% |

|||

|

105.00 |

5.00% |

$11.50 |

15.00% |

|||

|

110.00 |

10.00% |

$13.00 |

30.00% |

|||

|

110.10 |

10.10% |

$13.03(2) |

30.30% |

|||

|

120.00 |

20.00% |

$13.03 |

30.30% |

|||

|

130.00 |

30.00% |

$13.03 |

30.30% |

|||

|

140.00 |

40.00% |

$13.03 |

30.30% |

|||

|

150.00 |

50.00% |

$13.03 |

30.30% |

|||

|

160.00 |

60.00% |

$13.03 |

30.30% |

| (1) |

The hypothetical Beginning Worth of 100 utilized in these examples has been chosen for illustrative functions solely, and doesn’t symbolize a probable precise Beginning Worth for the Market Measure. |

|

(2) |

The Redemption Quantity per unit can not exceed the hypothetical Capped Worth. |

Redemption Quantity Calculation Examples

|

Instance 1 |

|

|

The Ending Worth is 80.00, or 80.00% of the Beginning Worth: |

|

|

Beginning Worth: |

100.00 |

|

Ending Worth: |

80.00 |

|

|

= $8.00 Redemption Quantity per unit |

|

Instance 2 |

|

|

The Ending Worth is 103.00, or 103.00% of the Beginning Worth: |

|

|

Beginning Worth: |

100.00 |

|

Ending Worth: |

103.00 |

|

|

= $10.90 Redemption Quantity per unit |

|

Instance 3 |

|

|

The Ending Worth is 130.00, or 130.00% of the Beginning Worth: |

|

|

Beginning Worth: |

100.00 |

|

Ending Worth: |

130.00 |

|

|

= $19.00, nevertheless, as a result of the Redemption Quantity for the notes can not exceed the hypothetical Capped Worth, the Redemption Quantity will likely be $13.03 per unit |

Danger Elements

There are vital variations between the notes and a standard debt safety. An funding within the notes entails important dangers, together with these listed under. It is best to fastidiously evaluate the

extra detailed rationalization of dangers referring to the notes within the “Danger Elements” sections starting on web page PS-6 of product complement EQUITY ARN-1, web page S-1 of the MTN prospectus complement, and web page 1 of the prospectus recognized above. We additionally urge

you to seek the advice of your funding, authorized, tax, accounting, and different advisors earlier than you spend money on the notes.

Construction-related Dangers

| ◾ |

Relying on the efficiency of the Market Measure as measured shortly earlier than the maturity date, your funding could lead to a loss; there isn’t any assured return of principal. |

| ◾ |

Your return on the notes could also be lower than the yield you would earn by proudly owning a standard fastened or floating charge debt safety of comparable maturity. |

| ◾ |

Funds on the notes are topic to our credit score danger, and precise or perceived adjustments in our creditworthiness are anticipated to have an effect on the worth of the notes. If we turn out to be bancrupt or are unable to pay our obligations, you could lose your |

| ◾ |

Your funding return is restricted to the return represented by the Capped Worth and could also be lower than a comparable funding straight within the Market Measure or the securities held by the Underlying Fund. |

Valuation- and Market-related Dangers

| ◾ |

The preliminary estimated worth of the notes is an estimate solely, decided as of a specific cut-off date by reference to our and our associates’ pricing fashions. These pricing fashions contemplate sure assumptions and variables, together with |

| ◾ |

The general public providing worth you pay for the notes will exceed the preliminary estimated worth. In the event you try and promote the notes previous to maturity, their market worth could also be decrease than the worth you paid for them and decrease than the preliminary |

| ◾ |

The preliminary estimated worth doesn’t symbolize a minimal or most worth at which we, MLPF&S, BofAS or any of our associates could be prepared to buy your notes in any secondary market (if any exists) at any time. The worth of |

| ◾ |

A buying and selling market will not be anticipated to develop for the notes. None of us, MLPF&S or BofAS is obligated to make a marketplace for, or to repurchase, the notes. There is no such thing as a assurance that any celebration will likely be prepared to buy your notes at any |

Battle-related Dangers

| ◾ |

Our enterprise, hedging and buying and selling actions, and people of MLPF&S, BofAS and our respective associates (together with trades in shares of the Underlying Fund or the securities held by the Underlying Fund), and any hedging and buying and selling |

| ◾ |

There could also be potential conflicts of curiosity involving the calculation agent, which is BofAS. We’ve the precise to nominate and take away the calculation agent. |

Market Measure-related Dangers

| ◾ |

The sponsor and advisor of the Underlying Fund could alter the Underlying Fund in a approach that would adversely have an effect on the worth of the notes and the quantity payable on the notes, and these entities don’t have any obligation to think about your |

| ◾ |

You should have no rights of a holder of shares of the Underlying Fund or the securities held by the Underlying Fund, and you’ll not be entitled to obtain securities or dividends or different distributions by the issuers of these securities. |

| ◾ |

Whereas we, MLPF&S, BofAS or our respective associates could occasionally personal the Market Measure or the securities held by the Underlying Fund, we, MLPF&S, BofAS and our respective associates don’t management the Underlying Fund or |

| ◾ |

There are liquidity and administration dangers related to the Underlying Fund. |

| ◾ |

The efficiency of the Market Measure could not correlate with the efficiency of the securities held by the Underlying Fund in addition to the online asset worth per share of the Underlying Fund, particularly in periods of market volatility when |

and the market worth of shares of the Underlying Fund and/or the securities held by the Underlying Fund could also be adversely affected, typically materially.

| ◾ |

The funds on the notes won’t be adjusted for all company occasions that would have an effect on the Underlying Fund. See “Description of the ARNs—Anti Dilution and Discontinuance Changes Regarding Underlying Funds” starting on web page PS-26 |

| ◾ |

There could also be potential conflicts of curiosity involving the calculation agent, which is BofAS. We’ve the precise to nominate and take away the calculation agent. |

Tax-related Dangers

| ◾ |

The U.S. federal earnings tax penalties of the notes are unsure, and could also be adversarial to a holder of the notes. See “Abstract of U.S. Federal Earnings Tax Penalties” under and “U.S. Federal Earnings Tax Abstract” starting on web page PS-41 of |

Extra Danger Elements

An Funding within the Notes Is Topic to Dangers Related to the Gold and Silver Mining Industries.

All or considerably all the shares held by the GDX are issued by gold or silver mining firms. Because of this, the shares that may decide the

efficiency of the GDX are concentrated in a single sector. Though an funding within the notes won’t give holders any possession or different direct pursuits within the shares held by the GDX, the return on the notes will likely be topic to sure dangers

related to a direct fairness funding in gold or silver mining firms.

As well as, these firms are extremely depending on the worth of gold or silver, as relevant. These costs fluctuate broadly and could also be affected by quite a few elements. Elements affecting gold costs embrace financial

elements, together with, amongst different issues, the construction of and confidence within the international financial system, expectations of the longer term charge of inflation, the relative energy of, and confidence in, the U.S. greenback (the foreign money by which the worth of gold

is usually quoted), rates of interest and gold borrowing and lending charges, and international or regional financial, monetary, political, regulatory, judicial or different occasions. Gold costs can also be affected by trade elements comparable to industrial and

jewellery demand, lending, gross sales and purchases of gold by the official sector, together with central banks and different governmental companies and multilateral establishments which maintain gold, ranges of gold manufacturing and manufacturing prices, and short-term adjustments

in provide and demand due to buying and selling actions within the gold market. Elements affecting silver costs embrace basic financial tendencies, technical developments, substitution points and regulation, in addition to particular elements together with industrial and

jewellery demand, expectations with respect to the speed of inflation, the relative energy of the U.S. greenback (the foreign money by which the worth of silver is usually quoted) and different currencies, rates of interest, central financial institution gross sales, ahead gross sales by

producers, international or regional political or financial occasions, and manufacturing prices and disruptions in main silver producing international locations comparable to Mexico and Peru. The availability of silver consists of a mix of recent mine manufacturing and present shares of

bullion and fabricated silver held by governments, private and non-private monetary establishments, industrial organizations and personal people. As well as, the worth of silver has occasionally been topic to very fast short-term adjustments as a result of

speculative actions. Now and again, above-ground inventories of silver can also affect the market.

However, the GDX displays the efficiency of shares of gold and silver mining firms and never gold bullion or silver bullion. The GDX could under- or over-perform gold bullion and/or silver

bullion over the time period of the notes.

The Notes Are Topic to Change Fee Danger.

As a result of securities held by the GDX are traded in currencies apart from U.S. {dollars}, and the notes are denominated in U.S. {dollars}, the quantity payable on the notes at maturity could also be uncovered to fluctuations within the trade

charge between the U.S. greenback and every of the currencies by which these securities are denominated. These adjustments in trade charges could replicate adjustments in numerous non-U.S. economies that in flip could have an effect on the cost on the notes at maturity. An

investor’s web publicity will depend upon the extent to which the currencies by which the related securities are denominated both strengthen or weaken towards the U.S. greenback and the relative weight of every safety.

The Underlying Fund

All disclosures contained on this time period sheet concerning the Underlying Fund, together with, with out limitation, its make-up, methodology of calculation, and adjustments in its

parts, have been derived from publicly accessible sources. The knowledge displays the insurance policies of, and is topic to vary by, Van Eck Associates Company (“Van Eck”). Van Eck, which licenses the

copyright and all different rights to the Underlying Fund, has no obligation to proceed to publish, and should discontinue publication of, the Underlying Fund. The results of Van Eck discontinuing publication of the Underlying Fund are mentioned in

the part entitled “Description of the ARNs—Anti-Dilution and Discontinuance Changes Regarding Underlying Funds” starting on web page PS-26 of product complement EQUITY ARN-1. None of us, the calculation agent,

MLPF&S, or BofAS accepts any accountability for the calculation, upkeep or publication of the Underlying Fund or any successor Underlying Fund.

The VanEck Vectors® Gold Miners ETF (“GDX”)

The GDX is an funding portfolio maintained, managed and suggested by Van Eck. The VanEck VectorsTM ETF Belief is a registered open-end funding firm that

consists of quite a few separate funding portfolios, together with the GDX.

The GDX is an trade traded fund that trades on NYSE Arca underneath the ticker image “GDX.”

The GDX seeks to supply funding outcomes that correspond typically to the worth and yield efficiency, earlier than charges and bills, of the NYSE Arca Gold Miners Index (the

“Underlying Index”). The Underlying Index was developed by the NYSE Amex and is calculated, maintained and revealed by NYSE Arca. The Underlying Index is a modified market capitalization-weighted index comprised of publicly traded firms concerned

primarily in mining for gold or silver.

The GDX makes use of a “passive” or “indexing” funding method in trying to trace the efficiency of the Underlying Index. The GDX will spend money on all the securities which

comprise the Underlying Index. The GDX will usually make investments no less than 95% of its complete property in widespread shares that comprise the Underlying Index.

The notes usually are not sponsored, endorsed, offered or promoted by Van Eck. Van Eck makes no representations or warranties to the homeowners of the notes or any member of the general public concerning the advisability

of investing within the notes. Van Eck has no obligation or legal responsibility in reference to the operation, advertising and marketing, buying and selling or sale of the notes.

The NYSE Arca Gold Miners Index

The Underlying Index is a modified market capitalization weighted index comprised of securities issued by publicly traded firms concerned primarily within the mining of gold or silver. The Underlying Index was developed

by the NYSE Amex and is calculated, maintained and revealed by NYSE Arca.

Eligibility Standards for Index Parts

The Underlying Index contains widespread shares, ADRs or GDRs of chosen firms which can be concerned in mining for gold and silver and which can be listed for buying and selling and electronically quoted on a serious inventory market

that’s accessible by overseas buyers. Typically, this contains exchanges in most developed markets and main rising markets, and contains firms which can be cross-listed, i.e., each U.S. and Canadian listings. NYSE Arca will use its discretion

to keep away from exchanges and markets which can be thought of “frontier” in nature or have main restrictions to overseas possession. The Underlying Index contains firms that derive no less than 50% of their revenues from gold mining and associated actions (40%

for firms which can be already included within the Underlying Index). Additionally, the Underlying Index will preserve an publicity to firms with a big income publicity to silver mining along with gold mining, which won’t exceed 20% of the

Underlying Index weight at every rebalance.

At the moment, solely firms with a market capitalization of better than $750 million which have a median each day buying and selling quantity of no less than 50,000 shares and a median

each day worth traded of no less than $1 million over the previous three months are eligible for inclusion within the Underlying Index. Beginning in December 2013, for firms already included within the Underlying Index, the market capitalization requirement at

every rebalance will likely be $450 million, the typical each day quantity requirement will likely be no less than 30,000 shares over the previous three months and the typical each day worth traded requirement will likely be no less than $600,000 over the previous three months.

NYSE Arca has the discretion to not embrace all firms that meet the minimal standards for inclusion.

Calculation of the Underlying Index

The Underlying Index is calculated by NYSE Arca on a worth return foundation. The calculation relies on the present modified market capitalization divided by a divisor. The divisor was decided on the preliminary

capitalization base of the Underlying Index and the bottom stage and could also be adjusted because of company actions and composition adjustments, as described under. The extent of the Underlying Index was set at 500.00 on December 20, 2002 which is the

index base date. The Underlying Index is calculated utilizing the next method:

The place:

t = day of calculation;

N = variety of constituent equities within the underlying index;

Qi,t = variety of shares of fairness i on day t;

Mi,t = multiplier of fairness i;

Ci,t = worth of fairness i on day t; and

DIV = present index divisor on day t.

Underlying Index Upkeep

The Underlying Index is reviewed quarterly to make sure that no less than 90% of the Underlying Index weight is accounted for by index parts that proceed to fulfill the preliminary eligibility necessities. NYSE Arca could at any

time and occasionally change the variety of securities comprising the group by including or deleting a number of securities, or changing a number of securities contained within the group with a number of substitute securities of its selection, if in NYSE

Arca’s discretion such addition, deletion or substitution is important or applicable to keep up the standard and/or character of the Underlying Index. Components will likely be faraway from the Underlying Index throughout the

quarterly evaluate if both (1) the market capitalization falls under $450 million or (2) the traded common each day shares for the earlier three months is lower than 30,000 shares and the typical each day traded worth for the earlier three months is

lower than $600,000.

On the time of the quarterly rebalance, the element safety weights (additionally known as the multiplier or share portions of every element safety) will likely be modified to evolve to the next asset

diversification necessities:

| (1) |

the burden of any single element safety could not account for greater than 20% of the entire worth of the Underlying Index; |

| (2) |

the element securities are cut up into two subgroups-large and small, that are ranked by market capitalization weight within the Underlying Index. Massive securities are outlined as having a beginning index weight |

| (3) |

the ultimate mixture weight of these element securities which individually symbolize greater than 4.5% of the entire worth of the Underlying Index could not account for greater than 45% of the entire index worth. |

The weights of the parts securities (taking into consideration anticipated element adjustments and share changes) are modified in accordance with the Underlying Index’s diversification guidelines.

Diversification Rule 1: If any element inventory exceeds 20% of the entire worth of the Underlying Index, then all shares better than 20% of the Underlying Index are lowered to

symbolize 20% of the worth of the Underlying Index. The combination quantity by which all element shares are lowered is redistributed proportionately throughout the remaining shares that symbolize lower than 20% of the index worth. After this

redistribution, if another inventory then exceeds 20%, the inventory is about to twenty% of the index worth and the redistribution is repeated.

Diversification Rule 2: The parts are sorted into two teams, massive are parts with a beginning index weight of 5% or better and small are parts with a weight of

underneath 5% (after any changes for Diversification Rule 1). The massive group will symbolize within the mixture 45% and the small group will symbolize 55% within the mixture of the ultimate index weight. This will likely be

adjusted by means of the next course of: The load of every of the big shares will likely be scaled down proportionately (with a flooring of 5%) in order that the mixture weight of the big parts will likely be lowered to symbolize 45% of the Underlying

Index. If any massive element inventory falls under a weight equal to the product of 5% and the proportion by which the shares had been scaled down following this distribution, then the burden of the inventory is about equal to five% and the parts with weights

better than 5% will likely be lowered proportionately. The load of every of the small parts will likely be scaled up proportionately from the redistribution of the big parts. If any small element inventory exceeds a weight equal to the product of 4.5%

and the proportion by which the shares had been scaled down following this distribution, then the burden of the inventory is about equal to 4.5%. The redistribution of weight to the remaining shares is repeated till your complete quantity has been redistributed.

Modifications to the Underlying Index composition and/or the element safety weights within the Underlying Index are decided and introduced previous to taking impact. These adjustments usually turn out to be efficient after the shut of buying and selling on the third Friday

of every calendar quarter month in reference to the quarterly index rebalance. The share portions of every element safety within the index portfolio stays fastened between quarterly critiques besides within the occasion of sure forms of company actions

comparable to inventory splits, reverse inventory splits, inventory dividends, or comparable occasions. The share portions used within the Underlying Index calculation usually are not usually adjusted for shares issued or repurchased between quarterly critiques. Nonetheless, within the occasion

of a merger between two parts, the share portions of the surviving entity could also be adjusted to account for any inventory issued within the acquisition. NYSE Arca could substitute securities or change the variety of securities included within the Underlying

Index, primarily based on altering circumstances within the trade or within the occasion of sure forms of company actions, together with mergers, acquisitions, spin-offs, and reorganizations. Within the occasion of element or share amount adjustments to the index portfolio,

the cost of dividends apart from atypical money dividends, spin-offs, rights choices, re-capitalization, or different company actions affecting a element safety of the Underlying Index, the index divisor could also be adjusted to make sure that there are

no adjustments to the index stage because of nonmarket forces.

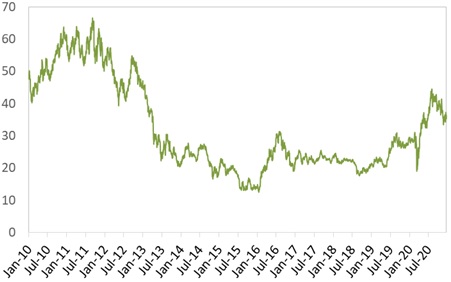

The next graph exhibits the each day historic efficiency of the Underlying Fund on its major trade within the interval from January 1, 2010 by means of December 23, 2020. We obtained this historic

knowledge from Bloomberg L.P. We’ve not independently verified the accuracy or completeness of the knowledge obtained from Bloomberg L.P. On December 23, 2020, the Closing Market Value of the Underlying Fund was $35.92. The graph under could have

been adjusted to replicate sure company actions comparable to inventory splits and reverse inventory splits.

Historic Efficiency of the Underlying Fund

This historic knowledge on the Underlying Fund will not be essentially indicative of the longer term efficiency of the Underlying Fund or what the worth of the notes could also be. Any historic upward

or downward development within the worth per share of the Underlying Fund throughout any interval set forth above will not be a sign that the worth per share of the Underlying Fund is kind of prone to improve or lower at any time over the time period of the

notes.

Earlier than investing within the notes, you must seek the advice of publicly accessible sources for the costs and buying and selling sample of the Underlying Fund.

Complement to the Plan of Distribution

Underneath our distribution settlement with BofAS, BofAS will buy the notes from us as principal on the public providing worth indicated on the quilt of this time period sheet, much less the indicated underwriting low cost.

MLPF&S will buy the notes from BofAS for resale, and can obtain a promoting concession in reference to the sale of the notes in an quantity as much as the total quantity of underwriting low cost set forth on the quilt of

this time period sheet.

We could ship the notes towards cost therefor in New York, New York on a date that’s better than two enterprise days following the pricing date. Underneath Rule 15c6-1 of the Securities Change Act of 1934, trades within the

secondary market typically are required to settle in two enterprise days, except the events to any such commerce expressly agree in any other case. Accordingly, if the preliminary settlement of the notes happens greater than two enterprise days from the pricing date,

purchasers who want to commerce the notes greater than two enterprise days previous to the unique difficulty date will likely be required to specify various settlement preparations to stop a failed settlement.

The notes won’t be listed on any securities trade. Within the unique providing of the notes, the notes will likely be offered in minimal funding quantities of 100 items. In the event you place an order to buy the notes, you’re

consenting to MLPF&S and/or one among its associates appearing as a principal in effecting the transaction to your account.

MLPF&S and BofAS could repurchase and resell the notes, with repurchases and resales being made at costs associated to then-prevailing market costs or at negotiated costs, and these costs will embrace MLPF&S’s and

BofAS’s buying and selling commissions and mark-ups or mark-downs. MLPF&S and BofAS could act as principal or agent in these market-making transactions; nevertheless, neither is obligated to have interaction in any such transactions. At their discretion, for a brief,

undetermined preliminary interval after the issuance of the notes, MLPF&S and BofAS could supply to purchase the notes within the secondary market at a worth which will exceed the preliminary estimated worth of the notes. Any worth supplied by MLPF&S or BofAS for the

notes will likely be primarily based on then-prevailing market circumstances and different issues, together with the efficiency of the Market Measure and the remaining time period of the notes. Nonetheless, none of us, MLPF&S, BofAS or any of our respective associates is

obligated to buy your notes at any worth or at any time, and we can not guarantee you that we, MLPF&S, BofAS or any of our respective associates will buy your notes at a worth that equals or exceeds the preliminary estimated worth of the notes.

The worth of the notes proven in your account assertion will likely be primarily based on BofAS’s estimate of the worth of the notes if BofAS or one other of its associates had been to make a market within the notes, which it isn’t obligated to do.

That estimate will likely be primarily based upon the worth that BofAS could pay for the notes in gentle of then-prevailing market circumstances and different issues, as talked about above, and can embrace transaction prices. At sure instances, this worth could also be increased

than or decrease than the preliminary estimated worth of the notes.

The distribution of the Observe Prospectus in reference to these presents or gross sales will likely be solely for the aim of offering buyers with the outline of the phrases of the notes that was made accessible to buyers in

reference to their preliminary providing. Secondary market buyers mustn’t, and won’t be approved to, depend on the Observe Prospectus for info concerning RBC or for any goal apart from that described within the instantly previous

sentence.

An investor’s family, as referenced on the quilt of this time period sheet, will typically embrace accounts held by any of the next, as decided by MLPF&S in its discretion

and appearing in good religion primarily based upon info then accessible to MLPF&S:

| • |

the investor’s partner (together with a home companion), siblings, mother and father, grandparents, partner’s mother and father, kids and grandchildren, however excluding accounts held by aunts, uncles, cousins, nieces, nephews or any |

| • |

a household funding automobile, together with foundations, restricted partnerships and private holding firms, however provided that the helpful homeowners of the automobile consist solely of the investor or members of the |

| • |

a belief the place the grantors and/or beneficiaries of the belief consist solely of the investor or members of the investor’s family as described above; offered that, purchases of the notes by a belief typically |

Purchases in retirement accounts won’t be thought of a part of the identical family as a person investor’s private or different non-retirement account, apart from particular person retirement accounts (“IRAs”), simplified

worker pension plans (“SEPs”), financial savings incentive match plan for workers (“SIMPLEs”), and single-participant or homeowners solely accounts (i.e., retirement accounts held by self-employed people, enterprise homeowners or companions with no staff different

than their spouses).

Please contact your Merrill monetary advisor when you have any questions concerning the software of those provisions to your particular circumstances or assume you’re eligible.

Structuring the Notes

The notes are our debt securities, the return on which is linked to the efficiency of the Market Measure. As is the case for all of our debt securities, together with our market-linked notes, the financial phrases of the notes

replicate our precise or perceived creditworthiness on the time of pricing. As well as, as a result of market-linked notes lead to elevated operational, funding and legal responsibility administration prices to us, we usually borrow the funds underneath these notes at a

charge that’s extra favorable to us than the speed which we check with as our inside funding charge, which is the speed that we’d pay for a standard fastened or floating charge debt safety. This typically comparatively decrease inside funding charge, which

is mirrored within the financial phrases of the notes, together with the charges and expenses related to market-linked notes, usually leads to the preliminary estimated worth of the notes on the pricing date being lower than their public providing worth.

At maturity, we’re required to pay the Redemption Quantity to holders of the notes, which will likely be calculated primarily based on the $10 per unit principal quantity and can depend upon the efficiency of the Market Measure. So as to

meet these cost obligations, on the time we difficulty the notes, we could select to enter into sure hedging preparations (which can embrace name choices, put choices or different derivatives) with BofAS or one among its associates. The phrases of those

hedging preparations are decided by looking for bids from market individuals, together with MLPF&S, BofAS and its associates, and keep in mind quite a few elements, together with our creditworthiness, rate of interest actions, the volatility of the

Market Measure, the tenor of the notes and the tenor of the hedging preparations. The financial phrases of the notes and their preliminary estimated worth rely partly on the phrases of those hedging preparations.

BofAS has suggested us that the hedging preparations will embrace a hedging associated cost of roughly $0.05 per unit, reflecting an estimated revenue to be credited to BofAS from these transactions. Since hedging

entails danger and could also be influenced by unpredictable market forces, extra earnings and losses from these hedging preparations could also be realized by BofAS or any third celebration hedge suppliers.

For additional info, see “Danger Elements—Normal Dangers Regarding the ARNs” starting on web page PS-6 and “Use of Proceeds and Hedging” on web page PS-19 of product complement EQUITY ARN-1.

Abstract of Canadian Federal Earnings Tax Penalties

For a dialogue of the fabric Canadian federal earnings tax penalties referring to an funding within the notes, please see the part entitled “Tax Penalties—Canadian Taxation” within the prospectus dated September 7, 2018.

Abstract of U.S. Federal Earnings Tax Penalties

It is best to contemplate the U.S. federal earnings tax penalties of an funding within the notes, together with the next:

| ◾ |

There is no such thing as a statutory, judicial, or administrative authority straight addressing the characterization of the notes. |

| ◾ |

You agree with us (within the absence of a statutory, regulatory, administrative, or judicial ruling on the contrary) to characterize and deal with the notes for all tax functions as pre-paid cash-settled by-product contracts in respect of the |

| ◾ |

Underneath this characterization and tax remedy of the notes, a U.S. holder (as outlined on web page 41 of the prospectus) typically will acknowledge capital achieve or loss upon the sale or maturity of the notes. This capital achieve or loss typically |

| ◾ |

No assurance may be on condition that the Inner Income Service or any court docket will agree with this characterization and tax remedy. |

| ◾ |

Underneath present Inner Income Service steering, withholding on “dividend equal” funds (as mentioned within the product complement), if any, won’t apply to notes which can be issued as of the date of this pricing complement except such |

It is best to seek the advice of your individual tax advisor regarding the U.S. federal earnings tax penalties to you of buying, proudly owning, and disposing of the notes, in addition to any tax penalties arising underneath the legal guidelines of any state,

native, overseas, or different tax jurisdiction and the doable results of adjustments in U.S. federal or different tax legal guidelines. It is best to evaluate fastidiously the dialogue underneath the part entitled “U.S. Federal Earnings Tax Abstract” starting on web page PS-41 of

product complement EQUITY ARN-1.

The place You Can Discover Extra Data

We’ve filed a registration assertion (together with a product complement, a prospectus complement, and a prospectus) with the SEC for the providing to which this time period sheet relates. Earlier than you make investments, you must learn the Observe Prospectus, together with

this time period sheet, and the opposite paperwork that we’ve filed with the SEC, for extra full details about us and this providing. You might get these paperwork with out price by visiting EDGAR on the SEC web site at www.sec.gov. Alternatively, we, any

agent, or any seller collaborating on this providing will prepare to ship you these paperwork in the event you so request by calling MLPF&S or BofAS toll-free at 1-800-294-1322.

“Accelerated Return Notes®” and “ARNs®” are the registered service marks of Financial institution of America Company, the father or mother firm of MLPF&S and BofAS.

[ad_2]

Source link