[ad_1]

This piece from 30 December was posted with permission by Rhona O’Connell, Head of Market Evaluation for EMEA and Asia at StoneX Group. Please go to the StoneX Market Intelligence portal and contemplate subscribing for extra of Rhona and staff’s analysis.

The gold:silver ratio is a much-watched indicator within the valuable metals markets and is commonly traded as an entity in its personal proper. On this temporary examine we have a look at a collection of intervals by which the ratio has modified sharply, in addition to the longer, shallower intervals in between. The observations present that the connection just isn’t as predictable as would possibly at first be thought.

Due to silver’s twin nature, each as a valuable steel and as an industrial commodity (industrial demand usually constitutes 60% of worldwide silver fabrication demand—i.e. excluding jewelry, cash&bars, silverware and ETPs), it is usually legitimate to have a look at the silver:copper relationship, and gold:copper sometimes additionally comes underneath scrutiny. So we now have additionally checked out how the latter two ratios fared throughout the identical intervals that we’re with respect to gold and silver, and set them in opposition to financial and monetary developments to see if there’s any consistency.

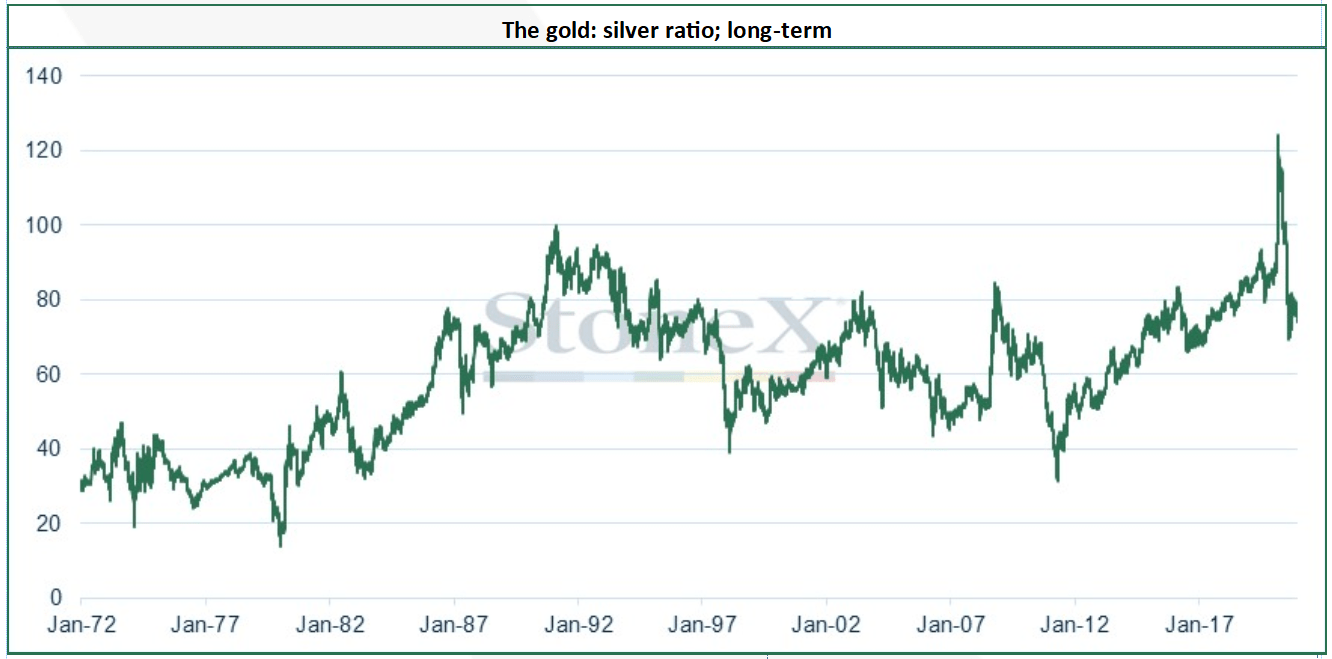

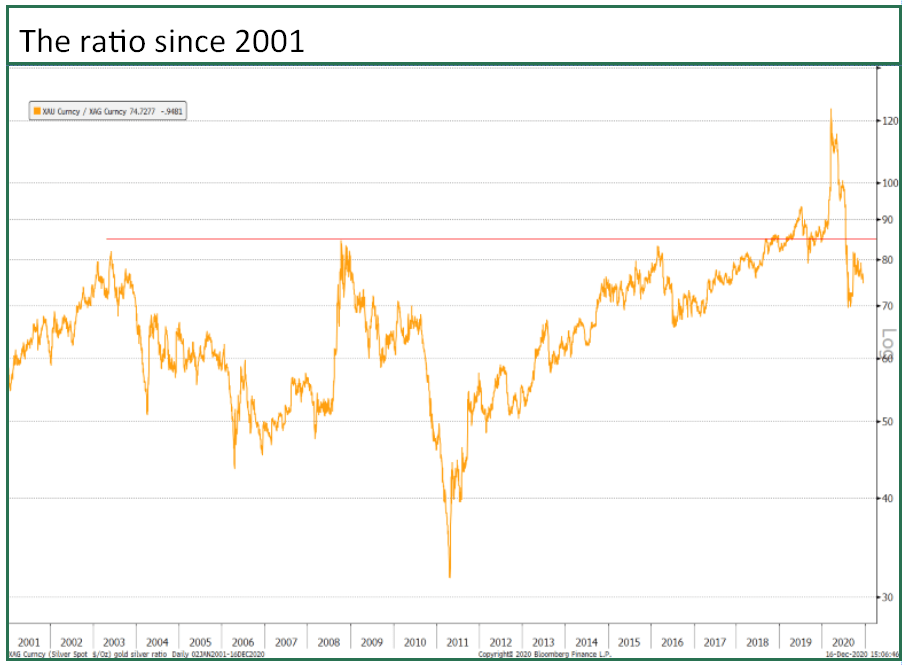

The chart under is a straightforward historic view of the gold:silver ratio for the reason that greenback got here off the gold normal. Overleaf we take a fairly extra technical view. The chart goes again to the beginning of 1972, which supplies gold slightly time to discover a impartial market worth after President Nixon closed the gold window on fifteenth August 1971. It was at that time that the two-tier system within the gold market was stopped. The London gold pool had collapsed in March 1968 within the face of relentless gold demand, and at this level the spot worth got here away from the beforehand mounted stage of $35/ounce and a two-tier system was developed, with central banks persevering with to commerce at $35/ounce. Finally this grew to become unmanageable, particularly as some banks have been shopping for gold on the central financial institution mounted worth, promoting it within the free market and taking the revenue. So the gold window was closed and the greenback began to drift free from $35. As an apart, the Federal Reserve nonetheless values its gold reserves at $42.22/ounce, the free market worth on the day the window was closed.

The ratio has averaged 59.6 for the reason that begin of 1972, with a low of 14.0 and peaking at 124.0 on 18th March as silver crumbled to eleven-year lows under $12 within the COVID meltdown, whereas gold was rallying from four-month lows. As we write the ratio has dropped under the important thing 72.0 stage, and, together with the basics, is sending fairly a robust sign for the subsequent transfer.

Supply: Bloomberg, StoneX

Supply: Bloomberg, StoneX

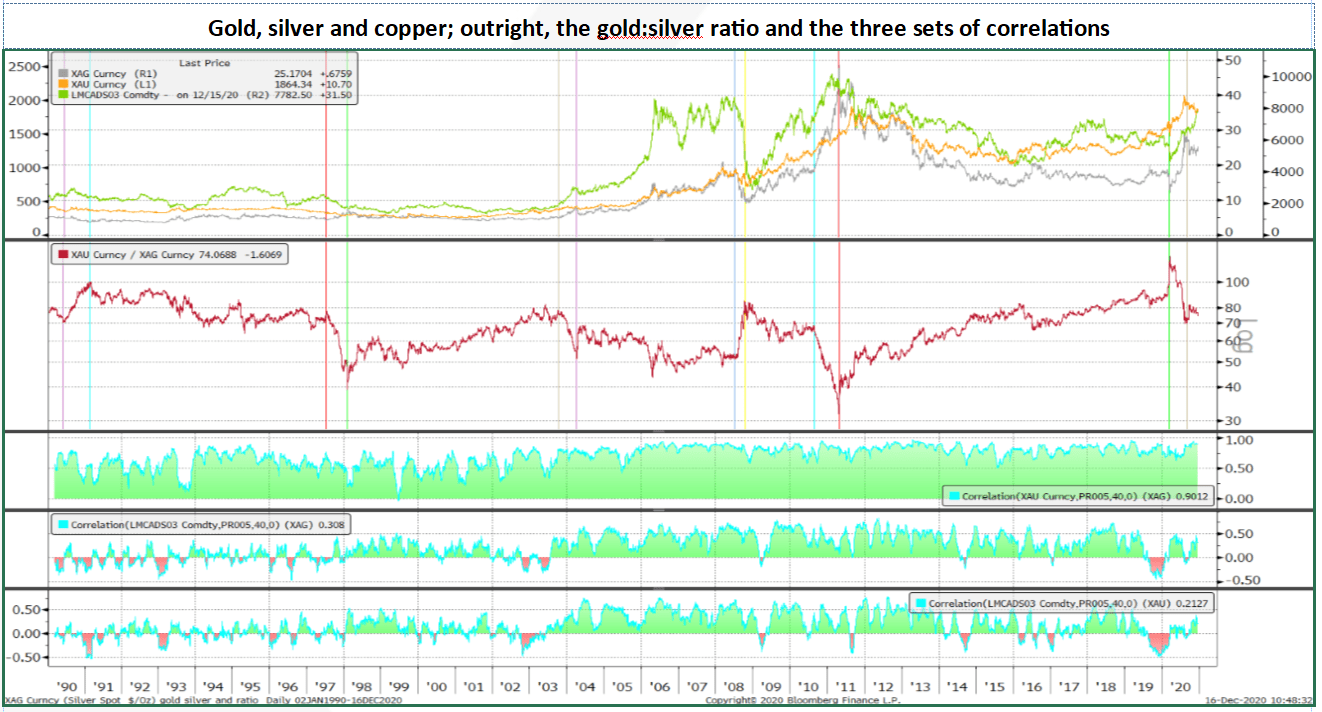

The chart above appears at gold, silver and copper from the beginning of 1990. The vertical strains spotlight the intervals when the gold:silver ratio modified sharply and these will be summarised into 4 contractionary intervals; three of those are related to a bull gold market, as needs to be anticipated given silver’s increased volatility in contrast with gold, however the first truly noticed gold in a light bear market. We come again to this additional on. There are two sharply expansionary intervals, each related to a bear gold market. In between, there are two intervals of gradual contraction and two of gradual enlargement.

So what do these intervals have in frequent, if something?

The Contractionary Phases:

- Weakening greenback; phases 2, 3, 4

- Fed steadiness sheet enlargement; phases 3,4

- Concern over fairness valuations; phases 2,4

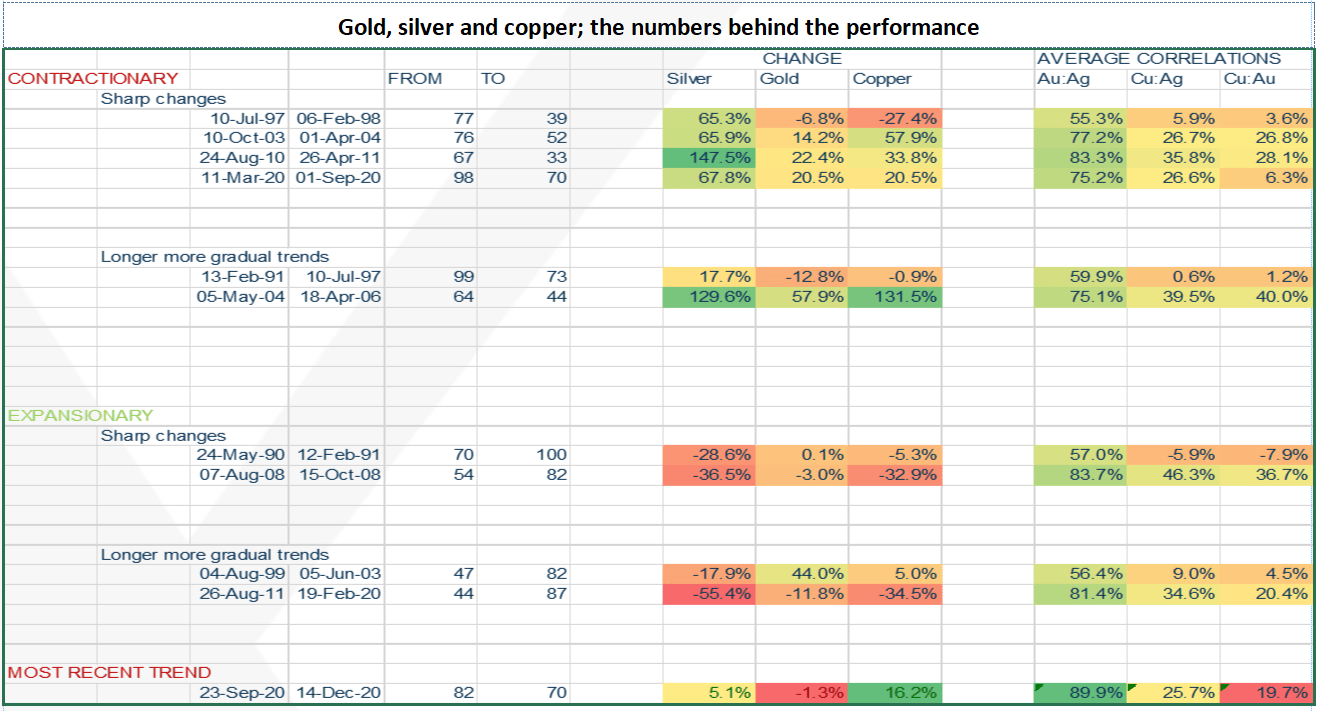

As famous, there are 4 of those. We’ll have a look at the earliest one final as it is rather a lot a one-off. The opposite three ran from October 2003 to April 2004, August 2010 to April 2011 after which the restoration from the meltdown earlier this 12 months, operating from March to September. As the next desk reveals, in all three instances the three metals moved in the identical course, with silver posting the biggest features and copper rating second (aside from this 12 months when gold and copper posted the identical will increase).

All three bull phases have a weakening greenback in frequent, with the latter two additionally characterised by enlargement of the Fed’s steadiness sheet (which after all would have an effect on the greenback); the second was the onset of QE2 (the second section of post-Lehman quantitative easing), whereas the Fed’s steadiness sheet exercise has been front-and-centre in monetary market sentiment this 12 months. The primary, whereas dollar-related, was additionally sure up with issues over the outlook for U.S. equities and the seek for various belongings. That is additionally related in 2020, with fairness valuations manner out of kilter, particularly given the unsure financial outlook, together with the surplus liquidity within the markets, which is trying to find a house. Gold is a beneficiary right here, and silver’s affiliation with gold and its increased volatility signifies that silver has reacted accordingly (notice the 8,000t-plus improve in silver ETPs this 12 months, equal to roughly 4 months’ international fabrication demand).

Supply: Bloomberg, StoneX

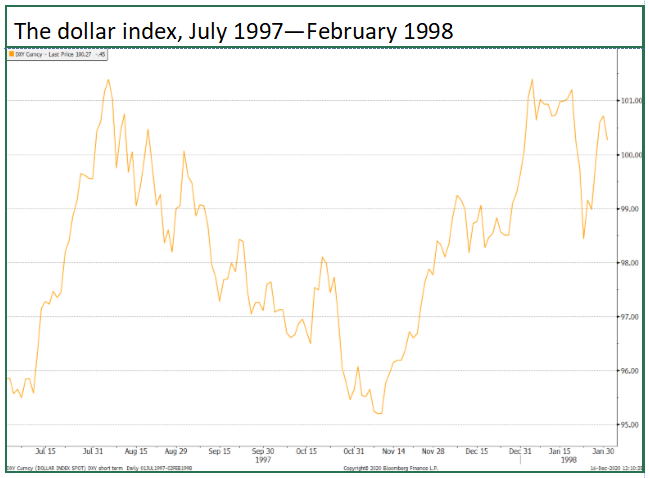

The outlier right here is, after all, section one. Between July 1997 and February 1998, the greenback was basically impartial (see chart under) and gold posted a small decline regardless of the East Asian forex disaster because the return of steel to the market and a big improve in liquidity saved the worth underneath some gentle stress by way of mine hedging together with brief promoting, whereas, importantly, sentiment was bruised by sporadic massive‑scale official sector gross sales.

Silver, nevertheless, recorded a 65% acquire, whilst copper dropped by 27%. Cue Mr Warren Buffett, the legendary investor, whose car Berkshire Hathaway began shopping for silver in late July 1997 and which by late January the next 12 months held 4,034t. Allied to this was a liquidity squeeze that at one level noticed lease charges in extra of 70%. Buffett was of the view that equilibrium between silver provide and demand would solely be achieved at increased costs and invested accordingly.

Supply: Bloomberg, StoneX

The Expansionary Phases

Þ Financial contraction

Within the first section, from Might 1990 to February 1991, gold was barely modified, whereas exhausting asset costs (and U.S. actual property) have been falling amid international GDP contraction. Gold remained comparatively strong on threat hedging, not simply from a monetary perspective, however geopolitical threat was necessary, with Iraq invading Kuwait. The well-publicised heavy gross sales from NCB Jeddah, reportedly to fund the acquisition of bombers, was comparatively well-taken, with the dangers within the Center East a stronger informer of sentiment.

The second section revolves across the monetary disaster in 2008, with Bear Stearns collapsing in March (and purchased by J P Morgan), the mid‑September collapse of Lehman Brothers and the following turmoil within the monetary sector. Gold’s marginal fall was as a result of legacy of misery promoting, whereas silver, unimpressed by gold’s obvious lack of efficiency, slipped additional, with the underperformance additionally inspired by the slide in copper.

Correlations

Which brings us onto the correlations between them of their three pairings. Keep in mind that “correlation” doesn’t essentially imply “course”.

It should come as no shock that silver’s relationship with gold is mostly significantly stronger than it’s with copper, averaging over 70% for the phases underneath statement. The common correlation with copper is simply over 20%. There isn’t any clear sample in that of silver:copper with financial circumstances, though the very best correlations do are typically when there are tangible adjustments in financial circumstances. This was most notable in 2008 when economies went into contraction, and in August-10/April-11 and Might-04/April-06, with confidence rising within the former case and development usually sturdy within the latter.

Total patterns; a very good indicator? Not likely

The formatting of the cells within the desk above helps to make clear the patterns available in the market strikes; the deeper the pink the decrease the quantity, as much as an intense inexperienced for the upper figures. Apparently there isn’t a repeat in any respect within the patterns of proportion adjustments in costs—the closest match is the latter two sharp contractionary phases, though even right here the hyperlink is tenuous, with copper outperforming gold within the third section however the two of them hand-in-hand within the remaining one.

Throughout the correlations there’s a barely tighter set of relationships, in that in eight situations from our pattern of 11, the correlation between copper and silver is increased than that between copper and gold. The exceptions have been within the intervals of very gradual contraction, however in neither case is the argument compelling. Within the first occasion, which was a interval of affordable financial development and comparatively low misery, the correlations themselves have been virtually non-existent. The second was in a interval of sturdy development, ending off with a collapse within the greenback, which might have knowledgeable the nearer relationships than within the earlier section.

And now?

Our present section, which is a contractionary one, displays gold and silver really fizzling out because the markets watch the vaccine developments and the tortuous progress in direction of recent financial stimulus. A key ingredient is copper outperforming the opposite two; that is partly a provide chain concern from earlier within the 12 months that’s nonetheless knocking on into the underlying fundamentals; the first focus although is the general base steel suite’s seeming confidence within the financial restoration in China and a few anticipation of eventual enchancment elsewhere. Silver, in the meantime, continues to be churned out as a by-product of different metals and is subsequently to some extent impervious to China’s exercise whereas gold is concentrating on threat urge for food

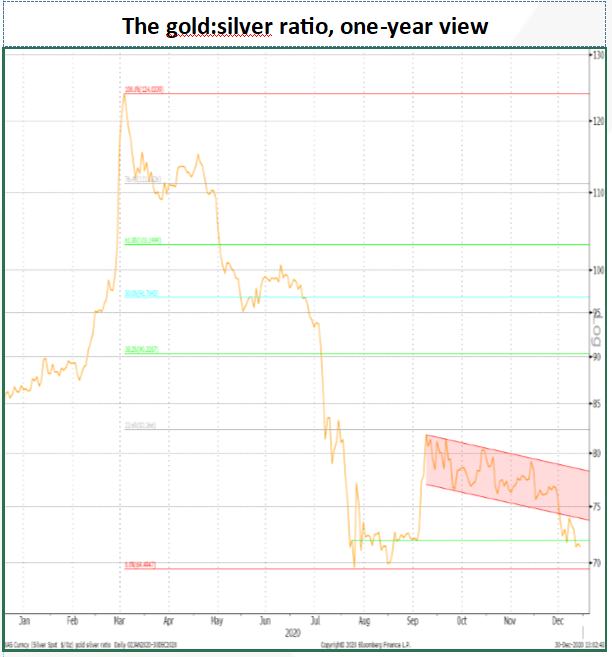

The technical view

Supply: Bloomberg, StoneX

Reversion to the long-term imply appears unattainable over any medium-term time horizon. A easy studying of congestion bands factors to a viable broad vary of 67 to 82, whereas a 2020 Fibonacci retracement factors to 82.4 because the higher stage of the band. Had been this to be damaged the subsequent goal could be 90.6. To the draw back, in a contractionary atmosphere, Fibonacci evaluation pegs assist at 67.8. So the Fibonacci and congestion analyses are kind of in keeping with each other.

Supply: Bloomberg, StoneX

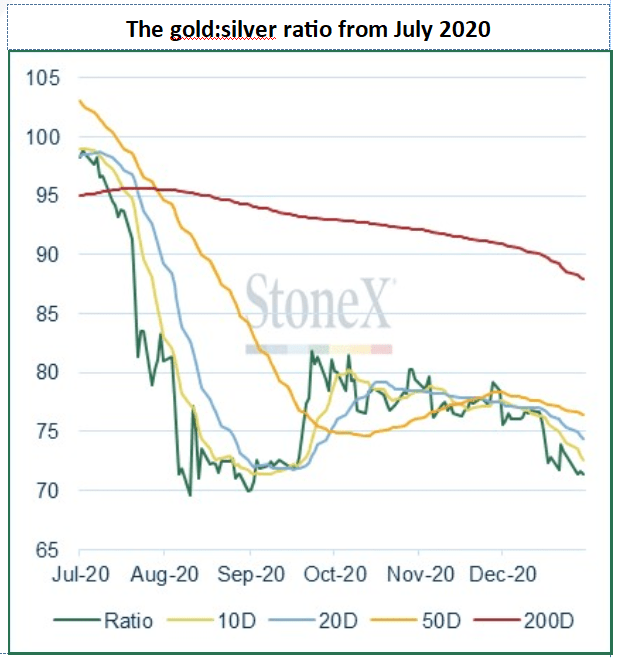

Within the brief time period the ratio has damaged under its latest downtrend, to face, as we write, at 71.4. For a pattern to be correctly damaged, the important thing assist space must be penetrated by 3%. So, because the ratio has now dropped to under 72.0, then that latest downtrend channel will begin to function resistance.

Supply: Bloomberg, StoneX.

In the meantime the transferring averages are in bearish formation for the brief time period, with the shortest common on the lowest and the longest, the very best. Sturdy resistance stands between 76.1 and 77.4.

Taking place?

Technical evaluation should all the time ignore the basics, however the identical doesn’t apply in reverse. The present constructions counsel that the ratio goes decrease. The basics counsel that gold goes increased. If this all comes about, then silver ought to outperform gold within the coming months. Section 4 to be reprised?

8.5.5

[ad_2]

Source link